Market Insight - May 2020

My theology professor at St. Thomas, when asked, “Why do bad things happen to good people?” replied, “So that we are able to appreciate that which is good”. There are of course so many different ways that he could have answered that eternal question, but that response has stuck with me since that day and helped me to put pain, anxiety and frustration into perspective. Likewise, it has aided in my sense of gratitude for all that is good in my life. Over the past several weeks, I have thought about this lesson often, countering moments of heightened stress with an appreciation for that which is good in my life.

On a normal, pre-COVID morning I’d be sipping on coffee and reading the paper alone at my desk in the office. Now with the office closed and all of us working from home, my 9-year-old son sprints to our mailbox each morning to retrieve the day’s paper for me. On most mornings we then sit down to breakfast together and listen to a recorded daily message from his school teacher regarding what’s in store for the day’s distance learning program. He’s teaching me how to do math (you know it’s different now, right?) and how to play Fortnite, while I am resisting the urge to give him a home haircut. In the chaos of the past several weeks and in light of this horrible virus, these moments and memories are what I’m grateful for, and I do find that it’s easy to appreciate them in the moment.

How to Anticipate a World After COVID-19

While we have been able to mostly turn off physical contact with other humans in fairly short order, the process of reversing that is likely to be much more complicated and drawn out. The brutal economics of stay-at-home orders are showing up across measurements of employment, spending, production, etc. The U.S. economy contracted by an estimated 4.8 percent1 during the first quarter of the year. More than 30 million people2 have filed for unemployment insurance since mid-March. Consumers, which account for about two-thirds of economic activity in the U.S., reduced their spending by 7.6 percent1 during the first quarter. The pressure in March and April was on keeping people separated. The pressure in May is likely to be on stemming the economic consequences of those stay-at-home orders. How successful we are at balancing health risks with economic risks is to be determined.

Moving forward is certain, but how is very uncertain. Despite what you read or hear, we are in a state of heightened uncertainty. Instead of trying to decide how the rest of this year will play out in the capital markets, it is likely better to realize that no one really knows. In the past month, I have listened to countless webcasts proclaiming that the recovery will look like a “U”, no a “V”, no actually it’ll look like a Nike Swoosh or a square root symbol. No one knows and to think otherwise is to suffer from one of the oldest follies in decision-making: overconfidence.

Learn from the Past to Prepare for the Future

It’s not to say that you simply throw up your hands and hope for the best. There is much to be analyzed and learned from how the markets reacted to the outbreak of COVID-19. The reaction from the Federal Reserve and other foreign central banks, as well as fiscal intervention in the U.S. and abroad, also provides meaningful information. It’s necessary to consider the intersecting crisis in the energy markets when attempting to learn from what has happened. An oversupply of oil and an abrupt drop in global demand led to cascading energy prices, momentarily sending the price for future delivery of crude oil below zero. No, that doesn’t mean gas stations will soon be paying you to fill up. It was more a reflection of how undesirable adding more oil to already burgeoning stockpiles was.

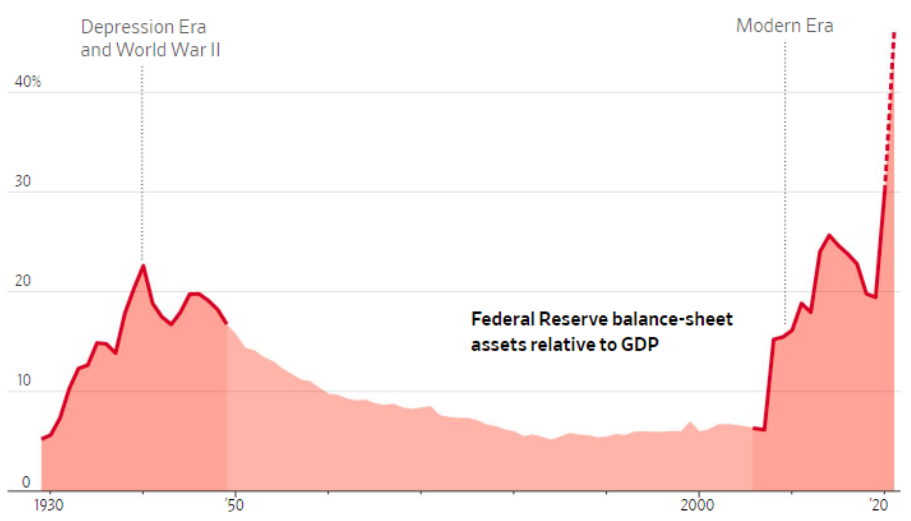

Perhaps the most important investment-related development to come from the current economic crisis is that global central banks are nearly unilaterally going to step in to defend asset prices when deemed necessary. The fact that the Federal Reserve is willing to act in this manner is not new. The scale and speed in which the Federal Reserve has acted this year is new, though. In Chart 1, you can see that the current response by the Federal Reserve will end up dwarfing all other stimulative actions taken in the past, including during the Great Depression. This can be seen as a good thing in that we know to expect this reaction. We can see that the Federal Reserve will provide a backstop to the U.S. economy and capital markets in nearly limitless scale. Yet, it does also raise significant concerns that are also not new.

Chart 1

Monitoring Federal Intervention and Managing Risk

Among the concerns is the future inflationary risk that such government spending might generate. That concern certainly hasn’t been validated since the last time the Federal Reserve significantly increased spending during the Great Recession. If anything, we’ve been more at risk of deflation than inflation over the past decade. Another concern is that the Federal Reserve will run out of ammunition to support the economy if another crisis emerges. This was a popular concern just three months ago, before the current economic crisis was on anyone’s radar. Since then, the Federal Reserve has demonstrated that it has considerable fire power remaining and isn’t afraid to use it.

Ultimately, what we worry about is what the Federal Reserve’s actions do to investment decision-making. How does an investor evaluate risk when central banks with unlimited spending potential are poised to step in to protect against losses in certain circumstances? How does an investor determine which investments are likely to be supported by central banks and which may be allowed to fail? Is significant monetary stimulus beneficial in the long run for investors, or will it ultimately decrease long-term returns for investors and impede economic growth?

Many questions emerge and while there isn’t a shortage of opinions, we know that no one really knows the answers. At their most basic level, investment decisions are always made without knowing the future. The present situation is no different. When we invest, we accept risk. Whether it be risk of losing nominal value (the actual value of your investment decreases) or losing real value (the value of your investment doesn’t keep up with inflation), we are always accepting some level of risk. In creating and managing your investment portfolio, we are attempting to seek the best long-term outcome for the risk that is being taken.

Appreciating the Good That's Still Here

We are at a point in an investment cycle that is dangerous for investors. Heightened uncertainty puts investors in a vulnerable position and may lead to poor decisions. Layer on top of that the anxiety induced by the health risks of COVID-19, and investors are particularly prone to misjudging the future. Remember that there is a reason we invest the way that we do. It is because the future is always uncertain. Asset values fluctuate for varying reasons. Economies grow and contract. These are expected events. So when they occur, more often than not, the best course of action is to stick to the plan that was in place before the crisis.

As is always the case, we are at Birchwood for one reason, and that is to serve you. Many mornings in the past two months as the sun rose, the birds began to emerge, trees began to bud and the pace of the day hadn’t quickened yet, I have reflected gratefully on the relationships that we have with each of you. We are all witnessing something quite profound, and I hope that it comes to an end soon and with you and your loved ones safe and healthy. Until then, know that we are available to you if you need us. Stay safe. Keep others safe. Appreciate the incidental consequences of sheltering at home and all that is good in your life.

Table 1

| Market Indices (as of 3/31/20) | 1st Quarter | One Year |

| Dow Jones Industrial Average | -22.7% | -13.4% |

| NASDAQ Composite | -14.0% | +0.7% |

| S&P 500 Index | -19.6% | -7.0% |

| Barclays Capital Aggregate Bond Index | +3.2% | +8.9% |

| Small Cap Stock (Russell 2000 Index) | -30.6% | -24.0% |

| Non-US Stock (MSCI EAFE Index) | -22.8% | -14.4% |

Gratefully yours,

Steve Dixon, CFA®

Investment Manager

Kay Kramer, CFP®, Dana Brewer, CFP®, Bridget Handke, CFP®, Damian Winther, CFP®, Rachel Infante, CFP®, Stacey Nelson, CFP®

Sources

1 Source: U.S. Bureau of Economic Analysis. https://www.bea.gov/news/2020/gross-domestic-product-1st-quarter-2020-advance-estimate. accessed April 29, 2020.

2 Source: Chaney, Sarah and King, Katie. “Over 3.8 Million Americans Filed for Jobless Benefits Last Week as States Struggle With Coronavirus Claims Surge”. https://www.wsj.com/articles/states-struggle-with-coronavirus-unemployment-claims-surge-11588239004?mod=hp_lead_pos1. accessed April 30, 2020.

Chart 1 Source: Timiraos, Nick and Hilsenrath, Jon. “The Federal Reserve Is Changing What It Means to Be a Central Bank.” The Wall Street Journal; April 27, 2020; https://www.wsj.com/articles/fate-and-history-the-fed-tosses-the-rules-to-fight-coronavirus-downturn-11587999986; accessed April 29, 2020.

Table 1 Source: Morningstar. Market indexes are unmanaged and investors cannot invest directly in indexes. However, these indexes are accurate reflections of the performance of the individual asset classes shown. All returns reflect past performance and should not be considered indicative of future results.