Market Insight - October 2016

With considerably less animosity or entertainment value, there is another major debate raging at the moment that doesn’t involve our choices for the next U.S. president. It is one that is perennial, has been analyzed exhaustively by scholars and has staunch advocates at opposite sides of the debate. The conflicting wisdom of Warren Buffett illustrates why investors can’t seem to make a clear determination on whether passive or active investing is the superior methodology.

Mr. Buffett has been famously quoted as saying that investors “should try to be fearful when others are greedy and greedy when others are fearful”1. This comment seems to advocate for an active investment approach, encouraging investors to separate from the crowd. Nearly ten years later, he wrote that his bequeathed assets should be invested in a stock-based index fund and short-term government bonds2. It doesn’t get much more passive than that.

What is Active Investing?

We should back-up briefly to define what passive and active investing is. A passive investment approach is one that attempts to mirror the performance of a basket of securities or a market index, such as the S&P 500 Index. Active investment is when an investor seeks to be selective in their allocation to securities based on a strategy or philosophy that they believe will perform better than simply investing in the general market. Passive is generally characterized as being lower-cost. Active seeks to exploit perceived inefficiencies in the market by investing in securities that are expected to perform well and avoid ones that are not expected to perform well. Active does tend to be a more expensive strategy.

Many have misunderstood the purpose of Mr. Buffett’s advice regarding fear and greed. His words are not meant to admonish passive investing. In fact, his famous quote is offered as pacifying advice to investors that refuse to heed his initial guidance to simply invest passively in a “diversified, low-expense”1 index fund. Some call it humility and others call it arrogance, but Mr. Buffett has hardly walked his talk.

The first page of each of the Berkshire Hathaway Chairman’s Letters, which are published annually, compares the performance of the company’s investment portfolio relative to the S&P 500 Index. Mr. Buffett has exercised a philosophy of active investment, but advocated for passive investing among others. Perhaps he acknowledges his own exceptional skill and luck and, in an act of civic duty chooses not to lead the ordinary investor to believe a similar outcome is reasonable through active investment. In this respect we see his advice to invest passively in a low-cost index fund as being the humble advice of a uniquely successful investor.

Passive vs. Active

As one of the founding philosophical decisions for any investor, the passive versus active debate elicits passionate supporters in both camps. The reality is that most professional investors find themselves in favor of a combination of active and passive, not exclusively one or the other. The loudest voices come from the staunch advocates for one strategy over the other. As such, it may seem that investors choose active or passive and follow that methodology throughout their investment portfolio. In my experience, that is the exception rather than the rule.

Mr. Buffett’s advice to use a low-cost index fund is offered as a blanket recommendation, without consideration for time horizon, liquidity needs, risk tolerance or any of the other considerations that are imperative to offering prudent investment advice. We are fiduciaries for our clients and must act in your best interests based on our skill, knowledge and experience. In order to do so, we must take into account the unique needs, wants and constraints of each of you.

As was mentioned earlier, there has been extensive research on which strategy is better. It is not my intention to attempt to summarize or add to that body of knowledge in this letter, but rather to explain Birchwood’s philosophy.

Our Philosophy

However, these inefficiencies are more pervasive in certain areas of the capital markets. For example, we believe that the market for large, U.S.-based stocks is sufficiently efficient most of the time to warrant a primarily passive investment strategy. When we say efficient, we mean that publicly available information has been efficiently priced into the present value of a stock. So an active investor will have a difficult time consistently capitalizing on a dislocation between the market price of a stock and its intrinsic worth. As such, we don’t believe that it makes sense to invest your assets in a more expensive strategy that faces a difficult challenge of outperforming the market consistently over time. We will generally elect to invest in a lower-cost index fund.

When investing in bonds, there are notable differences that lead us to favor active management over passive for your portfolio. Bond indexes, on which passive investments are based, allocate more weight in the index to the larger issuers of bonds. This means that organizations that have issued the most debt represent a bigger slice of the index than smaller issuers. The commonly referenced Bloomberg Barclays US Aggregate Bond Index is comprised of 45 percent U.S. government-related bonds3. This methodology for weighting the index offers active investors an advantage that does not exist in stock market indexes, which are generally weighted based on the market value of the company. In the stock market, stocks that are growing more valuable represent a higher and higher weight in the index. In the bond market, bond issuers that are issuing more and more debt represent a higher and higher weight in the index.

In the bond market we also believe less efficient trading markets, over-reliance on the accuracy of bond rating organizations and more price insensitive market participants, such as central banks, offer better opportunities for the consistent outperformance of active investors.

We also seek to employ an active investment style when building a portfolio based on sustainable, responsible, impact (“SRI”) principles. This is an area of the investing community that has grown rapidly over the course of the last decade. Active investors are integrating traditional financial analysis with research on the sustainability of the franchise to arrive at a more complete assessment of a stock or bond’s expected risk or return potential. While there are opportunities to invest passively using SRI criteria, they tend to lack potential advantages of active investment, such as active engagement with the management of a company to promote improved business practices that may unlock value in the company or reduce enterprise risk. For more information on SRI investing, subscribe to our quarterly SRI-focused newsletter The Leaf by clicking here.

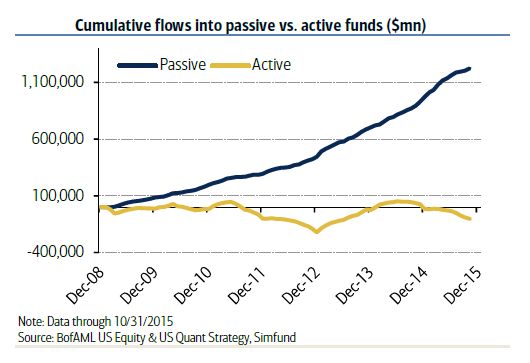

The trend has been toward passive investing across the board, in all asset classes. Over the past year investors have pulled $317 billion out of actively managed funds. At the same time, $373 billion has flowed to passively managed funds4. This trend extends back several years as Graph 1 illustrates. Investors have overwhelmingly favored passive over active during the past decade.

Graph 1

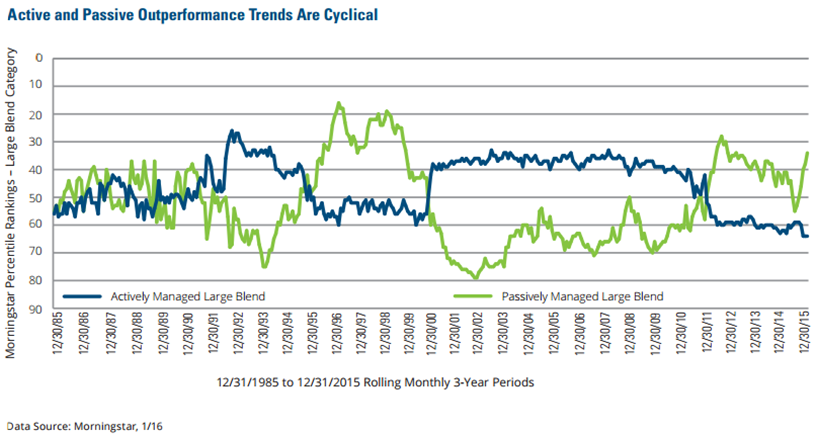

Here’s where some historical perspective may be helpful. The relative performance of active versus passive investments tends to be cyclical. In Graph 2, we see that active investments shined over passive for much of the 2000’s, only to see leadership switch to passive investments near the end of that decade.

Graph 2

Late into these cycles it is not uncommon to see rhetoric that denounces the efficacy of whichever strategy has been out of favor. Right now, it is easy to search the internet for recent articles predicting the demise of active investment. Likewise, financial product manufacturers are full-steam ahead in recent years developing new funds that cater to the investor that is solely focused on cost as the principal criterion for selecting investments.

We continually evaluate the prudence of investing with an active or passive approach in various asset classes. Capital markets evolve and change in some respects, which requires us to be open to reconsidering and challenging our beliefs periodically. At Birchwood, we take a blended approach to investing in active and passive strategies. Our interpretation of the research done on this topic and experience has led us to this conclusion. We believe that there are areas of the capital markets that offer reasonable opportunities for skilled investment managers to outperform a passive investment approach consistently over time after fees.

When we evaluate investments for inclusion in your portfolio, we are always taking into consideration the cost of the investment. It is part of our initial screening process, our ultimate investment selection decision and even factors into our ongoing management of your portfolio in so far as we seek to invest in the lowest cost share class available. As with other things in life, we are sometimes willing to pay more for quality if we believe it provides an advantage. In other situations, we see little value in paying more.

Advice is freely available and blasted at us in a myriad of ways. I use the Nike+ Run Club app on my iPhone when I run to track the distance that I’ve run, my pace and so on. As a reward for establishing an account with the app I periodically get advice about fitness, nutrition and general health topics, and of course I’m kept apprised of the latest technology in Nike running shoes. Some of this advice has been useful, but most has not been applicable to me.

Investment or financial advice is not dissimilar. Advice is easy to find, but most does not apply to you or may actually cause you harm if followed out of context. As a client of Birchwood, you understand this and see value in having a relationship with advisors that can offer guidance through the lens of your particular situation. We are exceptionally grateful to you and take this responsibility very seriously.

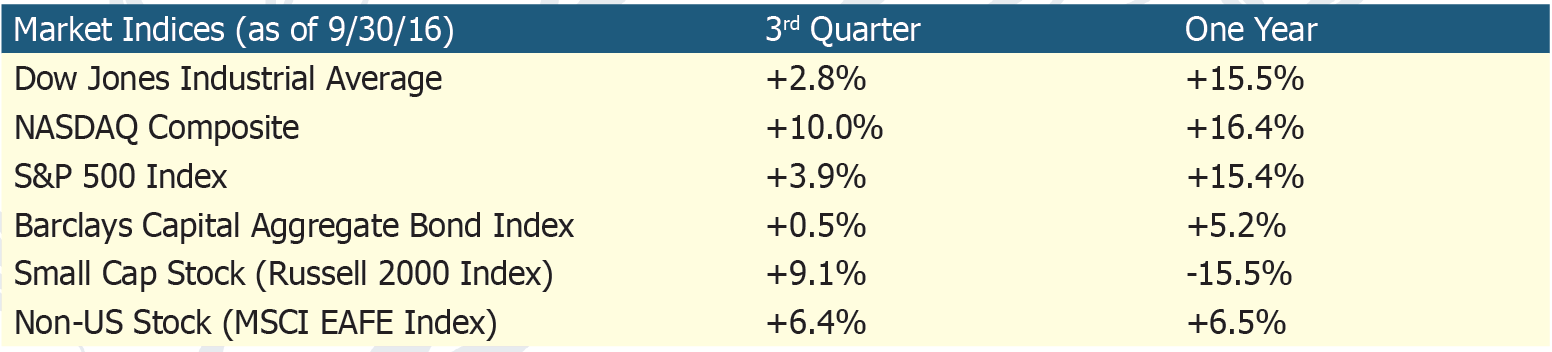

Table 1

If you know someone that is going through a transition in their life and may benefit from advice that takes their specific situation into consideration, please don’t hesitate to offer us as a resource. We often begin relationships during a period of personal transition, such as a job change, retirement, divorce or the passing of a loved one. There are many important decisions to be made during these periods and we welcome the opportunity to help provide some guidance and reassurance during what can be a stressful time.

1 Source: Berkshire Hathaway 2004 Chairman’s Letter www.berkshirehathaway.com/letters/2004ltr.pdf

2 Source: Berkshire Hathaway 2013 Chairman’s Letter www.berkshirehathaway.com/letters/2013ltr.pdf

3 Source: Bloomberg Barclays US Aggregate Index Factsheet, August 24, 2016 index.barcap.com/Home/Guides_and_Factsheets

4 Source: Morningstar Directsm Asset Flows Commentary: United States, data as of June 30, 2016 corporate.morningstar.com/US/documents/AssetFlows/AssetFlowsJul2016.pdf

Graph 1 Source: Bloomberg.com These Charts Show the Astounding Rise in Passive Management, by Julie Verhage, December 30, 2015. www.bloomberg.com/news/articles/2015-12-30/these-charts-show-the-astound...

Graph 2 Source: The Cyclical Nature of Active & Passive Investing, Hartford Funds www.hartfordfunds.com/dam/en/docs/pub/whitepapers/WP287.pdf

Investment Advisory services offered through Birchwood Financial Partners, Inc. an SEC Registered Investment Advisor.

All written content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Opinions expressed herein are solely those of Birchwood Financial Partners, Inc., and our editorial staff. Material presented is believed to be from reliable sources; however we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser or qualified professional before making any financial decisions. We are not affiliated with or endorsed by the Social Security Administration or any government agency. The inclusion of any link is not an endorsement of any products or services by Birchwood Financial Partners. All links have been provided only as a convenience.