Market Insight - November 2022

Until this year and with just a few minor exceptions, investing in traditional bonds has been a lucrative strategy for the past forty years. Traditional bonds have had an annual average return of 7.4%1 and relatively shallow downside risks. The worst peak-to-trough return until this year was -9% in 1981. Meanwhile, some years registered rich gains for investors, such as 1982 when bonds gained 33% and in 1995 when bonds appreciated by 19%. All told, bonds recorded positive returns to investors in 36 of the past 40 years with the worst calendar year loss being in 1994 when a bond investor lost 3% from January 1st to December 31st2. That context makes this year’s 15.7%3 decline in bonds almost unfathomable.

Bonds, Defined

Before we go too far, an explanation of what a bond is may be helpful. When an organization needs money, one method of raising it is by issuing a bond. A bond, like a loan, is a legal arrangement between the organization and a lender. The organization receives cash now to finance operations, build a factory, refinance another loan, etc. In most cases the lender receives interest payments and the return of the amount it lent, also known as principal, at some point in the future. The lender may decide to sell this bond, thereby transferring the right to receive its interest payments and return of principal to another party. The different details of the bond, the creditworthiness of the issuer, and the prevailing conditions of the capital markets will influence the price that is paid for the bond.

The yield of a bond is a calculation that includes the interest rate associated with that bond as well as other factors such as how long until the principal is paid back. Yield is also an estimation of the annual return of a bond until it matures. One of the primary capital market factors that will influence the yield of a bond is the general level of interest rates.

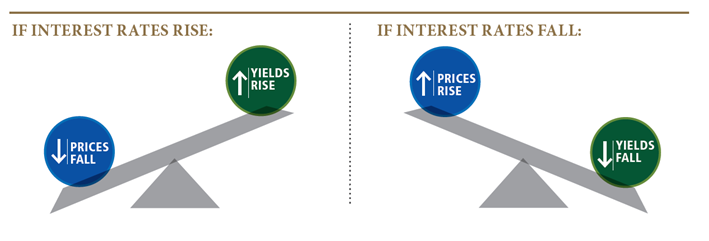

Image Source: PIMCO.com

You’ve maybe heard us explain that bond prices move inversely to interest rates or a bond’s yield. To illustrate this relationship, assume you buy a bond when it’s issued. The bond will pay an interest rate of 1%. If the level of general interest rates increased to 2% after you buy this bond, the price at which you can sell the bond will fall. This is because investors looking to buy bonds now have the option to buy a newly issued bond with a 2% interest rate, which would be more attractive than your bond paying only 1% in interest. To make your bond appealing to prospective buyers you’d have to lower the price at which you’d be willing to sell it. When you lower the price, the bond’s yield increases in order to entice a buyer to purchase it.

Interest Rates and Bonds

The general level of interest rates is heavily influenced by a group called the Federal Open Markets Committee (“FOMC”), which determines the level of interest charged for overnight lending between banks, also known as the federal funds rate. The level of the federal funds rate represents a base from which the capital markets will seek to determine the appropriate yield for bonds. As an example, at the end of last year, the yield on a U.S. government-issued bond that would mature in 5-years was 1.26%4. Fast-forward ten months and six meetings of the FOMC that resulted in increases in the federal funds rate, and that yield has climbed to 4.27%4. For context, the last time a 5-year U.S. government bond had a yield this high was in October 2007.

The FOMC has been raising the federal funds rate in an effort to calm inflation. Higher interest rates generally lead to less borrowing and spending, which may cool down demand for goods and services and allow price increases to moderate. The exceptionally fast pace that interest rates have risen this year has resulted in bond prices falling remarkably fast. This has caused a great deal of anxiety among investors as bonds are traditionally owned due to their relatively low risk and income-producing nature. When the stock market falls in value, bond investments are expected to perform better than stocks, buoying the overall value of one’s investment portfolio. Diversification, a key tenet of most investment philosophies including ours, has broken down this year. While it’s a harsh reminder that there are no guarantees in investing, we are not about to abandon diversification as the foundation of our investment strategy.

Long-Term Perspective

Another principle of investing that we espouse is a long-term perspective. Investing based on short-term expectations can lead to even more unpredictability of outcomes. Investment decisions that are based on near-term expectations are almost always heavily influenced by what has been happening in the markets. It is very difficult to make predictions about the direction of the markets over the next several months without projecting forward the recent past, whether consciously or subconsciously. At present, the tendency of a short-term investor may be to extrapolate further losses in bond investments because inflation is still a significant concern and the FOMC has made it clear that further increases in the federal funds rate would be coming. Yet, a long-term perspective may recognize the opportunity that bonds now present with lower prices and higher yields.

With higher interest rates, bonds now provide a higher level of income for investors. That higher level of income creates a positive skew to future bond market returns. Data from J.P. Morgan5 estimates that a further 1% increase in the level of interest rates could lead to a -0.3% total return on a government-issued 5-year bond. However, a 1% decrease in the level of interest rates could generate an 8.6% gain. While few expect interest rates to move lower in the near future, the asymmetry in upside versus downside is compelling to a long-term investor.

Taking it one step further, higher yields on bonds helps to reinstate their efficacy in a diversified portfolio. When yields were much lower, the expected return from bonds was also lower which meant they provided less support in a broadly invested portfolio if stocks lost value. Now, with higher yields, bonds may play a stronger diversification role moving forward. The loss in value from bond investments this year has not been pleasant and may lead us to consider them differently should interest rates fall back to the levels they were at last year. A common investing mistake at this time would be to abandon bond investments because of what has happened in the recent past instead of sticking to a longer-term perspective that suggests bonds offer the best yields that we’ve seen in about 15 years.

Table 1

| Market Indices (As Of 10/31/22) | Year-to-Date | One Year |

| Dow Jones Industrial Average | -8.4% | -6.7% |

| NASDAQ Composite | -29.3% | -28.6% |

| S&P 500 Index | -17.7% | -14.6% |

| Bloomberg Barclays Capital Aggregate Bond Index | -15.7% | -15.7% |

| Small Cap Stock (Russell 2000 Index) | -16.9% | -18.5% |

| Non-US Stock (MSCI EAFE Index) | -23.2% | -23.0% |

There has been a lot of news lately regarding economic recession and whether we’re in one or about to be in one. Please watch for another letter shortly on this topic as it is worthy of separating out and addressing. While many believe that a recession is determined by two consecutive quarters of negative economic growth, in reality that is just a generalization. Economic growth in the U.S. was negative in the first and second quarters of this year 6, but no recession has been declared. Still the risk that economic growth slips again as we head into 2023 and an official recession is experienced is a very real possibility, but not a given. We’ll discuss the risk of recession and what it means for the investment landscape. It’s important to know that economic recessions and bear markets are different, and they don’t begin and end at the same time.

Gratefully yours,

Steve Dixon, CFA® CSRIC®

Investment Manager

Dana Brewer, CFP®, Bridget Handke, CFP® CAP®, Damian Winther, CFP® CSRIC®, Rachel Infante, CFP® CSRIC®, Kimmie Moehring, CFP®

Sources:

1 Source: Morningstar, retrieved November 3, 2022. Annual average return for the Bloomberg US Aggregate Bond Index from February 1, 1980 to December 31, 2021 is +7.37%. Market indexes are unmanaged, and investors cannot invest directly in indexes. However, this index is an accurate reflection of the performance of the broad U.S. bond market. All returns reflect past performance and should not be considered indicative of future results.

2 Source: J.P. Morgan Asset Management, retrieved November 3, 2022. Bloomberg US Aggregate Bond Index annual returns and intra-year declines.

https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/guide-to-the-markets-slides-us/fixed-income/gtm-blusanualreturns/. Market indexes are unmanaged, and investors cannot invest directly in indexes. However, this index is an accurate reflection of the performance of the broad U.S. bond market. All returns reflect past performance and should not be considered indicative of future results.

3 Source: Morningstar, retrieved November 3, 2022. Market indexes are unmanaged, and investors cannot invest directly in indexes. However, this index is an accurate reflection of the performance of the broad U.S. bond market. All returns reflect past performance and should not be considered indicative of future results.

4 Source: Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 5-Year Constant Maturity, Quoted on an Investment Basis [DGS5], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS5, November 6, 2022.

5 Source: J.P. Morgan Asset Management, retrieved November 8, 2022. Fixed income market dynamics. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/?slideId=fixed-income/gtm-fiiyieldreturns.

6 Source: Gross Domestic Product, Third Quarter 2022 (Advance Estimate), October 27, 2022, https://www.bea.gov/sites/default/files/2022-10/gdp3q22_adv.pdf. Accessed November 8, 2022.

Table 1 Source: Morningstar. Market indexes are unmanaged, and investors cannot invest directly in indexes. However, these indexes are accurate reflections of the performance of the individual asset classes shown. All returns reflect past performance and should not be considered indicative of future results.