Market Insight - November 2017

Defying the expectations of many market pundits, the stock market has continued higher

in a nearly unchecked rise in 2017. The flawed, but tirelessly reported level of the Dow

Jones Industrial Average (“DJIA”) teased 18,000 in the days leading up to last November’s

elections. Fast-forward eleven months and the commonly used proxy for the U.S. stock

market has recently surpassed 23,000. Along the way, the DJIA has never lost more than

2 percent in a single day, never been down by more than 5 percent from its all-time high

at the time and has reset a fresh all-time high 59 times1. On average, the stock market

suffers an intra-year decline of about 14 percent2. It is very uncommon to have such a

placidly positive stock market.

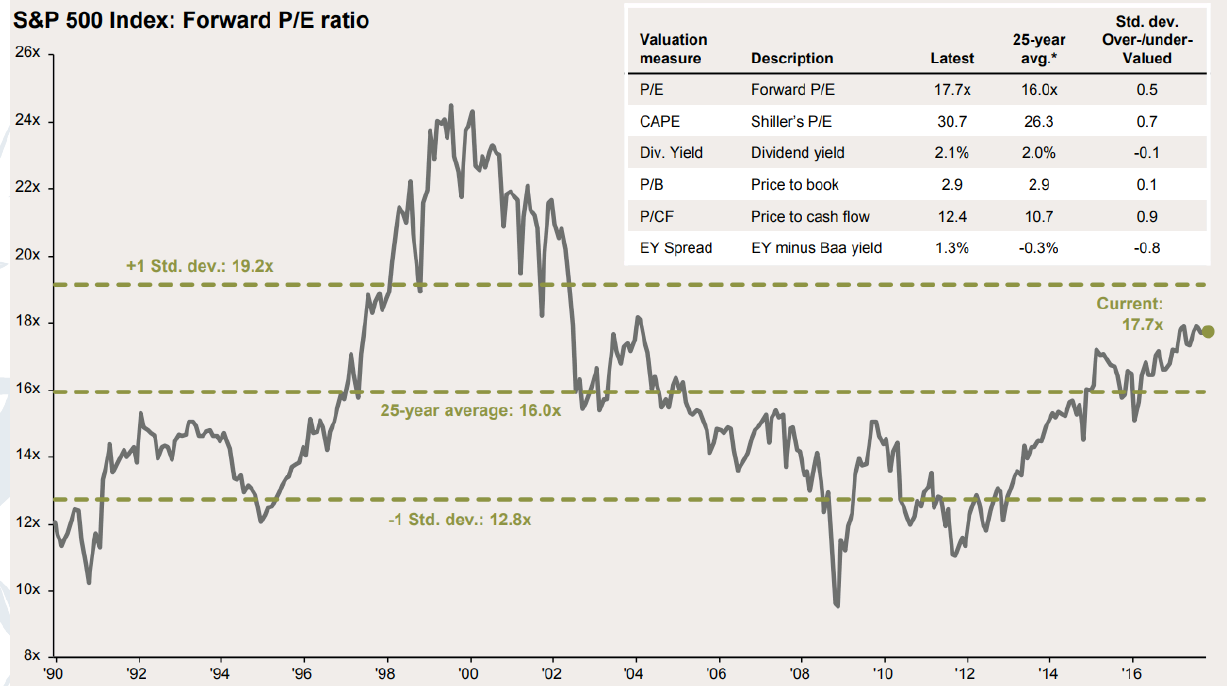

Chart 1

In Chart 1, the line represents how expensive stock prices are in relation to how much the companies represented by those stocks are earning in profits. There are many different ways to determine the fair value of a stock. Several of the other methods are shown in the table within Chart 1. There is no question that current valuations are above average, but it’s difficult to support an argument that valuations are extremely expensive. Interestingly, even if we assume that markets are overly expensive right now, the predictive power of that assumption over the near-term is questionable at best. Current stock valuations are a poor indicator of short-term market returns.

Why are Valuations Important?

If we can’t rely on valuations as a predictor of future returns, then why care about them at all? The reason is that valuations are important in estimating the future long-term returns for an asset class. It should be no surprise that buying a security when it’s relatively inexpensive is likely to result in a higher return over the long-term than buying the security when it’s relatively expensive. We can use current valuations to get a better understanding for what to expect from the stock market in terms of average returns over the next 5- to 10-years, but not over the next 5- to 10-months. In our opinion and based on the current level of valuations, we anticipate a relatively muted mid-to-high single-digit return from U.S. stocks over the next decade. That’s fairly sobering given that the average annual return for U.S. stocks has been about 10 percent over the past ninety years3. Still, our expectation is not for negative returns or returns that don’t outpace inflation over the long-term.

Even given this information, current valuations only explain about 40 percent of future 5-year returns of the stock market4. In other words, current valuations are not the lone determining factor in predicting long-term returns. We tend to pay a lot of attention to valuations, partly because of our experience in 2000. However, over the short-term, valuations are not very helpful in determining the direction of the stock market. Over the longer-term, the relationship between current valuations and future returns improves, but is still not entirely reliable.

Warren Buffett once said that “the stock market is a device to transfer money from the impatient to the patient”.

When we get to this part of the market cycle, there are two natural reactions that investors tend to have. Both reactions are reflected in Mr. Buffett’s comment as the impatient investor may either scramble to keep up or, conversely, attempt to sidestep an impending pullback in stock prices.

The fear of missing out, or “FOMO”, investor may increase risk in their portfolio by concentrating on the areas of the market that are performing the best. Separately, an investor may be driven by fear and a desire to avoid the next market collapse and will significantly decrease market risk in their portfolio. The FOMO investor believes that yesterday’s winners will be tomorrow’s winners. The fearful investor believes that yesterday’s gains will be tomorrow’s losses. Both can’t be right, but both can be wrong. Attempting to anticipate the direction of the stock market over the near-term is the best way to fall into Mr. Buffett’s classification of an impatient investor.

The Right Amount of Investing Confidence

There is no shortage of hubris in the investing community, but be careful not to mistake confidence with wisdom. We continue to believe that a disciplined strategy for investing your money that is focused on the longterm provides a better chance for achieving your goals than attempting to adjust allocations around near-term expectations. We don’t anticipate that this philosophy will land us a gig on CNBC anytime soon, but obviously our objective isn’t to entertain. Rather we take your financial goals seriously and apply what we believe is a tried and true method for helping you grow and protect your wealth over time and reach those goals.

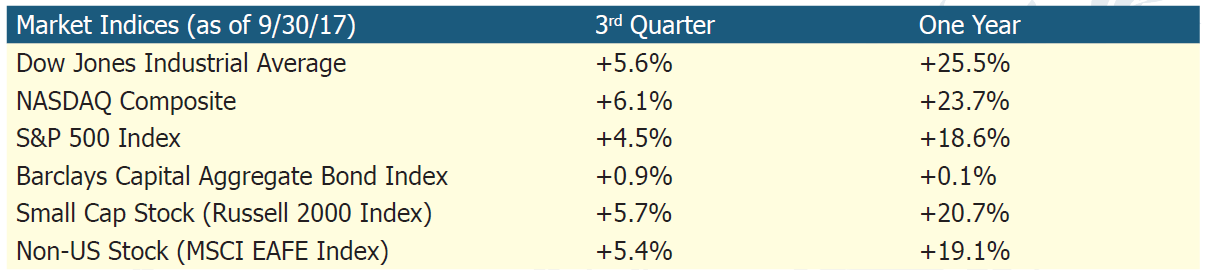

Table 1

It is with deep gratitude that I am pleased to provide you with this quarter’s Market Insight letter. I was shocked to realize that I have now been with Birchwood for ten years and this letter is the 40th that I have had the privilege to write. I would like to acknowledge and thank those of you that have been loyal readers as well as those of you that may be more casual readers. From the beginning, my hope has been to deliver a voice that is unique in this industry and that provides consistency and reassurance. Thank you for your conviction in Birchwood and the immensely talented and dedicated individuals that I have had the pleasure to work alongside for the past decade. As 2017 comes to an end, we wish you a happy and safe holiday season and look forward to seeing you again soon.

Gratefully yours, Steve Dixon, CFA, Investment Manager

1Source: Morningstar, Birchwood Financial Partners. Dow Jones Industrial Average values provided by Morningstar. Noted calculations by Birchwood Financial Partners.

2Source: Average return cited is for large stocks as represented by the Ibbotson® Large Company Stock Index from 1926 to 2016.

3Source: Davis, J., Ph.D., Aliaga-Díaz, R., Ph.D., Thomas, C. J., CFA. (October 2012). Forecasting stock returns: What signals matter, and what do they say now?

4Source: Davis, J., Ph.D., Aliaga-Díaz, R., Ph.D., Thomas, C. J., CFA. (October 2012). Forecasting stock returns: What signals matter, and what do they say now?

Chart 1

Source: J.P. Morgan Asset Management, FactSet, FRB, Thomson Reuters, Robert Shiller, Standard & Poor’s. See the J.P. Morgan Asset Management Guide to the Markets - U.S. - 4Q 2017 - as of September 30,2017 for additional relevant information.

Table 1

Source: Morningstar. Market indexes are unmanaged and investors cannot invest directly in indexes. However, these indexes are accurate reflections of the performance of the individual asset classes shown. All returns reflect past performance and should not be considered indicative of future results.