If you’re like most Americans, you may think that the day you retire is the day you turn on every retirement account you have contributed to throughout your career (401ks, Roths, etc.) as well as the funds you are now eligible to access, such as Social Security benefits.

However, many individuals fail to realize that switching on these income streams can be irrevocable, and if done at the wrong time, can permanently reduce your benefits in the long run. It's crucial to question how these diversified income sources will affect your tax payments in retirement, and to intentionally design a strategy that maximizes your income and supports your lifestyle needs.

How much cash flow will I need in retirement?

First and foremost, every family and individual has unique cash flow needs, and everyone's retirement looks different. What about yours? Do you plan to travel? To teach? To pick up new hobbies? Designing a retirement income stream created to fit your lifestyle while preparing for longevity takes careful planning – including planning for your projected income tax payments.

Should I collect Social Security before my Full Retirement Age?

Few people realize that collecting Social Security benefits before your Full Retirement Age (FRA) comes with its own problems. Not only do you take a permanent reduction in your Social Security retirement benefit (for life!), but you are also subject to the Annual Earnings Limit, which in 2020 is $18,240.

Putting this into context, if you begin collecting your Social Security retirement benefits before your FRA and you still have earned income from employment (even if only a part time job), you will give back $1 in benefits for every $2 in earnings above the Annual Earnings Limit.

Most retirees overlook this aspect of retirement, but it's very important: when you retire before your FRA, you not only lock in a permanently reduced lifetime retirement benefit, but a portion of this benefit may be withheld while you continue to earn income.

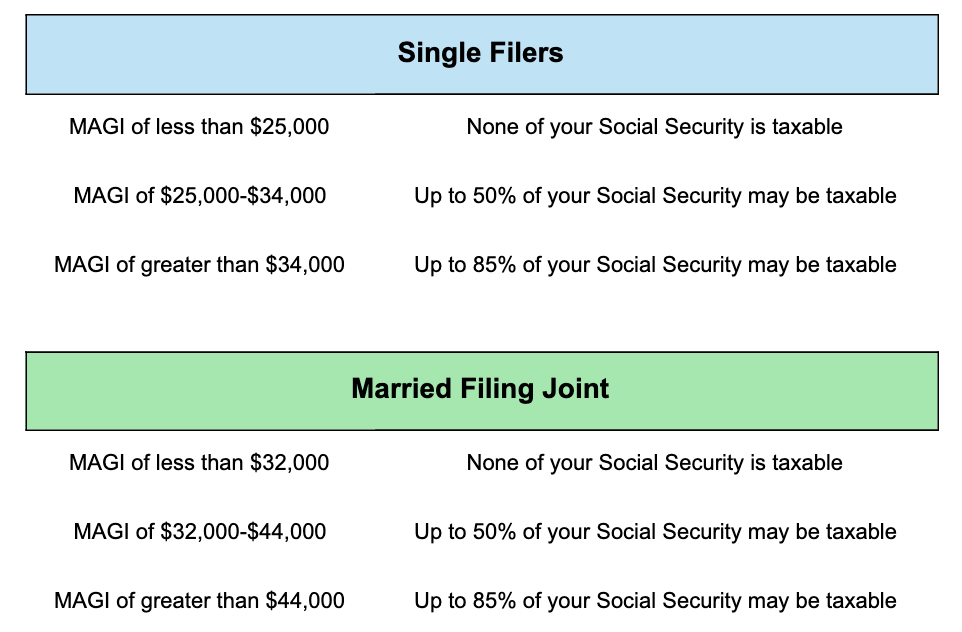

How are my Social Security benefits taxed?

Social Security benefits become taxable at different Modified Adjusted Gross Income (MAGI) thresholds. The calculation for MAGI is:

Adjusted Gross Income +

Tax Exempt Interest +

50% of Combined Social Security Benefits =

Modified Adjusted Gross Income

Depending on your MAGI, you may want to give some additional thought to controlling your retirement income sources in order to reduce the amount of Social Security retirement benefits that are subject to taxation. Thresholds for the taxability of Social Security retirement benefits are shown below:

Not only can additional earned or investment income subject more of your Social Security benefits to taxation, it may also push you into a higher marginal Federal and State income tax bracket. Understanding how your income streams will be taxed in retirement will help you design the best possible income distribution strategy for you and your family.

For example, if you're hovering near the top of the 12% marginal Federal income tax bracket with additional earned income, you could be pushed into the 22% marginal Federal income tax bracket AND up to 85% of your Social Security retirement benefits could be subject to taxation. Even a modest increase in MAGI could lead to a sizable tax bill.

Diversification is Key

When clients ask us for advice about retirement, we stress the importance of not letting the tax tail wag the dog – that is, not letting one factor influence the entire structure of your retirement plan. But taxes and income distribution strategies are critical to maintaining the longevity of an investment portfolio.

Diversification doesn’t just come in the form of asset allocation (i.e. stocks vs. bonds), it also affects how income is structured from different accounts and how these streams will be taxed throughout your retirement journey.

To review your specific situation, discuss with your financial advisor or visit the Social Security Administration website at ssa.gov to contact your local Social Security office.