There are a number of reasons why someone begins searching for a Financial Advisor. Maybe they want to start planning their path to retirement, they are overwhelmed with their retirement accounts from a previous and current employer, or they are considering what to do with a recent inheritance on top of a busy schedule.

There are a number of reasons why someone begins searching for a Financial Advisor. Maybe they want to start planning their path to retirement, they are overwhelmed with their retirement accounts from a previous and current employer, or they are considering what to do with a recent inheritance on top of a busy schedule.

Financial advisors can help simplify the complexities of your finances to help you make choices with confidence, and often provide plans specifically tailored to your goals and needs.

Since finances can be a very personal topic, it’s important to research firms to find the right fit. We’ve included a list of questions and topics to use as a guide when selecting a Financial Advisor.

1. What is your background and qualifications? Do you have any credentials such as a CFP, CFA, etc.?

Technical knowledge comes from education – that education could have been part of the advisor’s college curriculum, a certification program, such as a Certified Financial Planner™ (CFP®), or through experience.

For example, the CFP® demonstrates a commitment to the financial planning process, and candidates complete studies on many topics, including stocks, bonds, taxes, insurance, retirement planning, and estate planning. There are other certifications, some are much more rigorous and accepted in the industry than others. Investopedia has provided a list of common certifications:The Alphabet Soup of Financial Certifications.

While certifications are not everything, you should give extra credit to investment professionals who have them. Most of these certifications require candidates to put in many hours of study and meet high ethical and professional standards.

2. How long have you been an advisor?

Like most professions, it takes time to fully understand the many facets of the job. Experience matters.

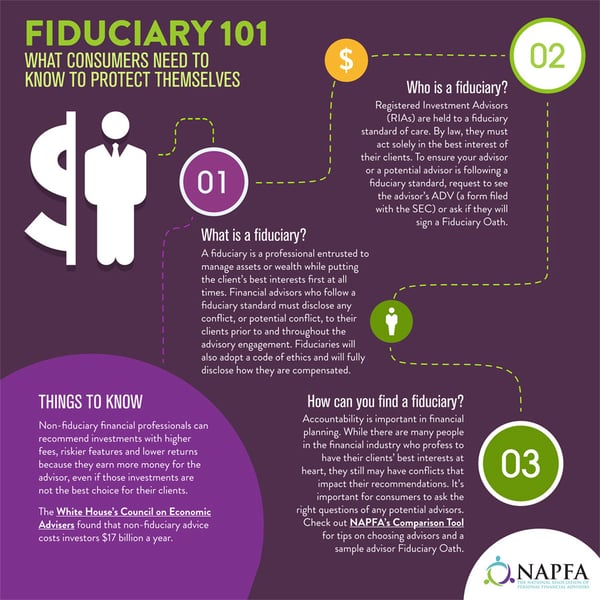

3. Are you a Fiduciary? Are you always a fiduciary?

The IRS defines Fiduciary to mean, “In general terms, a fiduciary is a person who owes a duty of care and trust to another and must act primarily for the benefit of the other in a particular activity.” In other words, is the financial advisor required to put your interests ahead of theirs?

In the financial planning industry advisors can be held to various standards depending on who regulates their business model. Some advisors are always Fiduciaries, some advisors can sometimes be held to a fiduciary standard and others are not a fiduciary at all.

Graph 1

4. Have you received any disciplinary infractions?

You may consider checking out discipline histories in advance of contacting any potential advisor. Most advisors discipline history can be found in one of the following regulatory sites.

a. SEC: https://www.sec.gov/check-your-investment-professional

b. FINRA: https://brokercheck.finra.org/

c. State Regulator

5. What services do you offer? Which service is your specialty?

Firms may specialize in a variety of ways. Some firms are investment only organizations; they are not focused on financial planning but exclusively manage your investments. Some firms are focused on small business owners helping them to set up retirement plans and benefit packages for their employees. Other firms focus on financial planning and provide investment advice to support your plan.

A firm may also have a specialty or two. For example, one of Birchwood’s specialties is Sustainable Responsible Impact Investing.

Understanding the typical client served by the firm will help you to know if you are a good fit.

6. How many clients do you have per advisor?

Depending on the level of service you desire and the level of technology and staffing the financial planning firm uses will determine the ratio of clients to advisors. Industry benchmarks typically say the optimal number is between 75 – 100 clients per advisor.

7. What is your client retention rate?

It is one thing to connect with an advisor at the beginning of a working relationship, but it’s equally important that the advisor continues to provide value over time. Retention rates can help to discern if the firm’s current client’s expectations are being met.

No firm is perfect and there will always be clients that leave for reasons beyond the advisor’s control. For example, a client moved to a new city and wants someone local, or a family member has gotten into the financial planning business and they want to give them a try.

8. What is your investment approach? (i.e. Low-cost index funds, active vs passive)

There are a lot of ways to manage investments and some of the important ones are that the firm can articulate their strategy, they pay attention to costs and they provide their clients with a performance report that compares your investment performance to an appropriate benchmark so you can know how your accounts are fairing.

9. Where do you get advice and support from when working on client plans?

This question is geared toward understanding the team the advisor has built around them. There are certainly some small firms that don’t have all of their resources on staff but have formed a community of resources.

10. Walk us through your retirement distribution planning process.

This question addresses the many facets of retirement planning. When the day has come that you need to create a “paycheck” using all of your retirement income sources as well as income from your investments, it is essential the advisor has a process to follow.

A big element of the process involves tax planning. There can be a variety of tax planning opportunities especially for those who retire before age 70. Look for firms that talk about the taxability of your various types of assets and income when they talk about their retirement distribution process.

11. What tools do you use to do planning?

For those of you who are still in the accumulation stage of retirement or getting close to retirement and want to understand if you have accumulated enough assets for financial independence, it is essential to work with your financial advisor to determine if your goals are likely attainable. Gone are the days the advisor puts your numbers into a program and spits out a long paper report telling you your retirement prognosis. Today, many advisors have goal planning tools that you do interactively in a meeting to fine tune the variables of your plan. Look for an advisor that will work with you to examine and educate you on the many elements and choices for your plan.

12. What is the involvement level after we become clients? Who will we be working with? How close to retirement are you?

Like all good relationships, it is important to establish expectations at the beginning of the relationship. Ask the advisor about:

a. The frequency of meetings (annual, quarterly). Tell them if you would prefer face-to-face, phone or online screen sharing.

b. Who will you work with –for financial planning, investing, paperwork, etc?

c. What is the firm’s game plan should something happen to the advisor. Is there a succession plan in place if the advisor is nearing retirement age or if there were an event that impacted the advisor’s ability to work?

13. How do you get paid?

There are three basic ways in which financial advisors are compensated. Each model has pros and cons:

a. Through a commission-based model

i. Advisors make a set amount every time they sell a certain product or service

b. Through a commission & fee model

i. Advisors charge an upfront fee to their clients and they can also earn a commission.

c. Through a Fee-Only model

i. Advisors earn their pay strictly from the fees they charge clients. They may charge a flat rate fee, an hourly rate, or calculate fees based on a percentage of assets they manage for a client.

14. Why do we want to work with you?

Each firm should have a good answer to this question. Only you can know if the answer resonates for you.